Should you open Trump accounts for your children?

The One Big Beautiful Bill Act of 2025 established a new type of account for children: the Trump account. Parents can opt in to these accounts for their children by including Form 4547 with their tax return this year or by visiting trumpaccounts.gov.

Children born 2025-2028 who have a social security number and one U.S. citizen parent with a social security number will receive a $1,000 “seed money” deposit from the federal government. Billionaire Michael Dell has also pledged to contribute $250 to these accounts for children under age 10 who live in zip codes with median household income under $150,000. Some large corporations have also pledged to match the government’s seed fund contribution for their employee’s children’s accounts.

Parents can contribute up to $5,000 per year to each child’s Trump account. An article in the Wall Street Journal (The Hack That Turns Trump Accounts Into Multimillion-Dollar Tax-Free Nest Eggs) on March 23 shows how parents with excess funds to invest can use Trump accounts to build a $3 million retirement nest egg for each of their children (AFTER saving for their own retirement and other shorter-term goals like college in other accounts). I was curious how this strategy compares to other types of accounts that you could fund for your children, so I did some math.

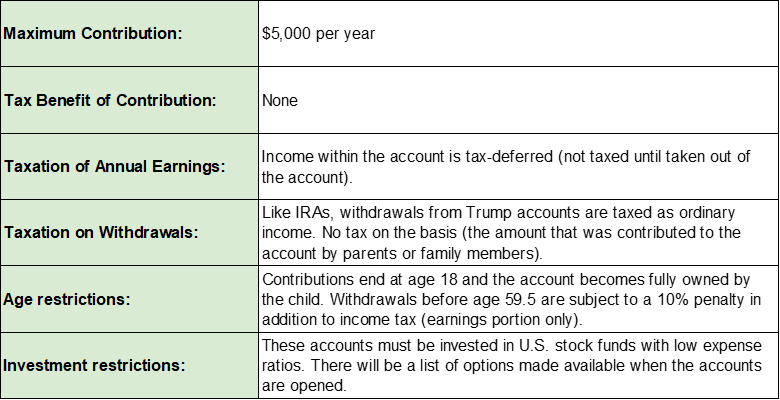

The Basics of Trump Accounts:

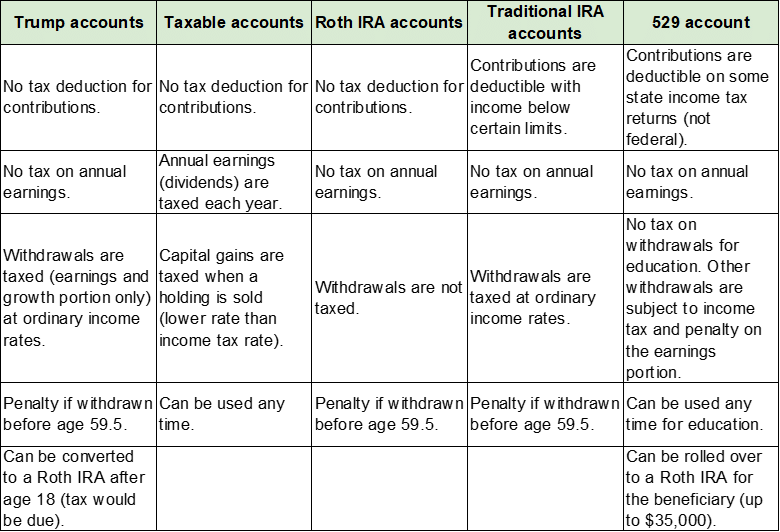

Before I go into the math comparing the illustrations from the Wall Street Journal article to other types of accounts, let’s take a moment to compare the taxation of Trump accounts with other accounts you could use.

The Hack Proposed by the Wall Street Journal Article

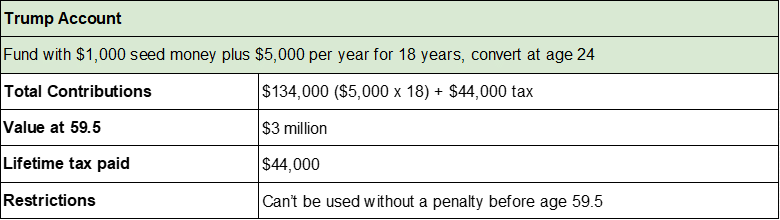

The article builds an illustration that assumes parents with enough cash flow (the author is careful to point out this is a lower priority than fully funding their own retirement accounts and other short to medium-term goals like education accounts) contribute $5,000 per year into Trump accounts for their children and then pay the income tax to convert the account to a Roth IRA around their child’s age 24. The reason the author chose age 24 for the conversion is that the child would not be a dependent by then, but would probably not have a very high income. This means that the account could be converted at a relatively low tax rate (compared to the parents’ tax rate). The tax would need to be paid from a source outside the account itself, so the assumption is that the parents would foot the tax bill for the child.

The illustration is built for children who are born this year or in the next two years, so they receive the seed money ($1,000) from the federal government and $5,000 per year from their parents in each of the first 18 years of their lives.

Assuming a 7% growth rate (a reasonable assumption for U.S. stock fund returns), the account would be worth about $278,000 when converted at the child’s age 24. This would result in a tax bill (to be paid by the parents) of about $44,000. Then the account would grow tax-free and could be used tax-free in the child’s retirement. The projected balance at the child’s age 59.5 is about $3 million, and they could use it tax-free. That is an amazing gift to give a child!

How does it compare to using a custodial taxable brokerage account for the child?

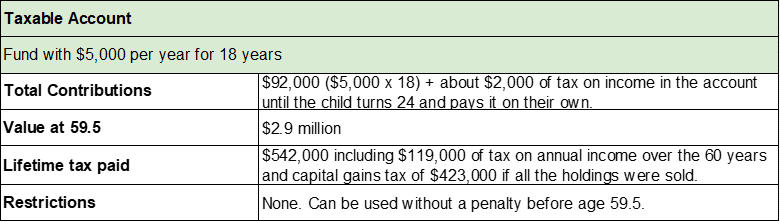

If you use a taxable brokerage account for your child (you are still the custodian until they reach the age of majority in your state– either 18 or 21), you will pay tax on the yearly income from dividends. If the account remains untouched until age 59.5, the value would still reach about $3 million. Instead of paying the $44,000 of tax to convert the account when the child is 24 years old, they would pay tax on the annual earnings and then a capital gains tax on any holdings sold to make a withdrawal.

While the child is a dependent, the first $1,350 of annual investment earnings (dividends) are untaxed, and the next $1,350 are taxed at the child’s rate (usually pretty low). If we assume (like the WSJ author did) that the value of the account will grow 7% per year in addition to the contributions of $5,000 per year for 18 years, we can estimate the annual taxable income on the account and the tax impact of selling holdings in retirement to take income. I assumed a dividend yield rate of 1.2%, which is reasonable for a U.S. stock fund. For the first 14 years, the annual income would be untaxed, as it would be less than the child’s standard deduction. We assume a kiddie tax rate of 10% on the dividends above $1,350 through age 22, then a 24% marginal tax rate when the child (perhaps optimistically) starts earning a solid income at age 23.

Finally, the child (who has now become a retiree), will pay capital gains tax on any shares that are sold from the account in order to take cash for income after age 59.5. Keep in mind, with a taxable account there is no need to wait until age 59.5. These funds could be used any time with no penalty. We are only assuming 59.5 to make a comparison with the Trump accounts in the WSJ article illustration.

With a taxable account, we are estimating an account value of $2.9 million at age 59.5 (it is only lower than the Trump account because it doesn’t get that $1,000 of seed money from the government), and total lifetime taxes of up to $542,000 if the account is fully used during the child’s lifetime. The estimated total lifetime taxes include $119,000 of tax paid on the annual dividend income in the account through the first 59.5 years and $423,000 of capital gains if all the holdings were sold at age 59.5. The actual tax would probably be less since the holdings would likely not be sold all at once.

How does it compare to using a Roth IRA?

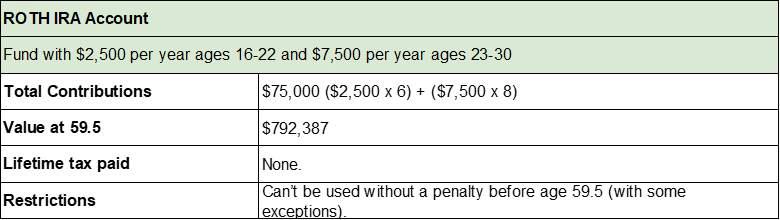

If you have the opportunity to contribute to a Roth IRA for your child, this is even better than the Trump account because you never have to pay to convert it. You can only contribute the amount that they make in earned income, which for children and teenagers is usually far less than $5,000 per year. On the other hand, they can contribute to a Roth IRA even past their 18th birthday (unlike a Trump account) and can contribute up to $7,500 per year (that is the limit for 2026, it increases with inflation). If you match your child’s earned income while they are in high school and college with Roth IRA contributions, and then make their Roth contributions for them after they begin their careers while their income is under the income limit (currently $153,000 for single individuals and $242,000 for married couples), you will be giving them a huge gift toward their retirement and it will not cost you any additional taxes.

Other considerations

- The math above shows that the Trump account “hack” suggested by the WSJ article is indeed pretty powerful– $3 million of tax free money for your child’s retirement is an amazing gift if you can afford the $5,000 contributions each year and the $44,000 tax bill when they are in their early 20s.

- Using a taxable account would result in a higher lifetime tax bill, but your child would get a lot more flexibility in exchange. A taxable account could be used without a penalty for a home purchase or their own child’s college education or any other need that they may have before age 59.5. Finally, the tax burden could be significantly less than the $542,000 estimate if they didn’t sell all the holdings in retirement or if the sales were timed to keep taxable income low.

- Another note about taxable accounts: If you keep the taxable account in your own name with a “Transfer on Death” to your child, you would pay the tax on the annual income, but then they would inherit the account and have the ability to sell all the holdings with no tax when they inherit the account (due to the “step in basis” on the date of death). So that is another highly income tax efficient way to set them up for retirement. This strategy gives the same flexibility in case you decide to let them use the funds early. The potential downside (upside) is that your child may be much older than 59.5 when they inherit the account. Another potential downside is that if the account is in your own name at your death, it would be included in your estate. Currently estates worth more than $15 million ($30 million for a married couple) are subject to estate tax. Not many people have to worry about that, even among those who can afford to fund these Trump accounts, but it is good to keep in mind.

- Making Roth IRA contributions for your child once they have earned income is another very powerful tool. The maximum contributions will be lower when they are a child (unless you have a very high earning minor) but you can continue to make the contributions in their adulthood until their income exceeds the limit for making direct Roth contributions. The upside here is that there is no additional tax!

- If you want us to give you personalized advice on what makes the most sense for your family, we are happy to do that!