The best habits are the ones you can stick with.

In January 2025, I made a phone call to a personal trainer at my local gym. I said, “I know I need to workout with weights, but I hate it.” I told her that I prefer to exercise outdoors, that I don’t get a mood boost from gym workouts like I do from running, and I like to exercise alone or with a friend instead of in a group class.

Despite my negativity, we set up an initial meeting and I committed to two 30-minute sessions with her per week. I found that it was pretty easy to show up since we had the appointments set, and it was really nice not to have to think about what to do. I didn’t even have to count my reps– she told me exactly what to do and when to stop. It helped that it was only 30 minutes, and only twice a week, and that she eased me in carefully. I didn’t miss a session except when I was traveling or she was traveling.

Fast forward to February 2026. One morning I was in the gym doing my workout and that day I was doing assisted pullups (with my right foot in a big elastic band attached to the bar to make them easier). There was a group of (extremely generous) ladies in the gym that morning who started cheering me on and acting very impressed. I think what I was doing looked harder than it was. Still, it felt great! And I did take a moment to celebrate how far I had come in a year’s time.

I thought, “Wow. I never would have thought someone would be impressed by watching me in a gym. And here I am after only 30 minutes twice a week.” At no point during the year were these workouts a major focus. It never felt like something I was putting a lot into or making a sacrifice to do, but doing it consistently added up to a significant result. If I had committed to three times per week or to hour-long sessions, I might not have been able to stay so consistent.

I think this is true across many areas of life. Anything that you do consistently will have inevitable effects. Maybe the trick is to not do so much that you can’t maintain the consistency. For example, it has been said that reading five stories to a young child each day will lead to them hearing about 1.5 million more words before kindergarten than a child who didn’t hear stories. Impressive and doable, right? Now if you increase that to reading 30 stories to a child each day, while the impact would be much greater, that would be too much– it would take away from playing outside and may burn you both out so that you give up reading altogether.

We see this all the time in financial planning and investing.

If you read our last article about whether it makes sense to contribute to Trump accounts for your children, you may have been struck by the projected balance of an account after making $5,000 contributions each year for 18 years. By age 59.5, the account would be worth $3 million! If you didn’t read the article, the gist is that saving regularly in any type of account will result in a surprisingly large sum if you do it consistently and leave it alone for a long time.

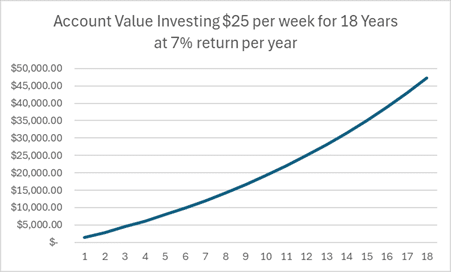

Even putting $25 per week into an account for 18 years will lead to nearly $50,000 with a 7% growth rate. A $25 weekly contribution may not feel like much, but having $50,000 to use for college or another goal would be very helpful! The fact that the $25 per week doesn’t feel like a sacrifice means that you probably won’t ever stop doing it, and won’t ever feel so burdened that you need to use the account early for some other goal.

Like having a standing appointment with a trainer, setting up an auto draft for that weekly $25 contribution will help you stay consistent.

Here are some ways we have seen clients make small, sustainable habits that have lead to significant growth:

- Make the minimum 401(k) contribution to get your full employer match and then increase your contribution by 1% per year until you are making the maximum deferral.

- If you don’t have a 401(k) at work, set up an auto draft into an IRA or a Roth IRA and contribute $100 per paycheck. Increase it when you can and let it grow until at least age 59.5.

- If you are in a high deductible health plan, make contributions to an HSA and try not use the funds for your copays or other medical costs. See if you can invest the HSA funds and leave them there until you turn 65.

- Start contributing to a college savings account when your child is born, even if it is only a small amount each month. You will be so glad you did when they are ready to take their educational journey beyond high school.

Consistency for the win! We are here to help, give us a call if we can help you make a small change to meet your goals.

Since you made it to the end, here is a picture of me doing my thing at the gym!