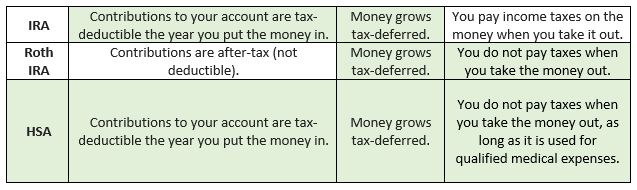

If you are looking for additional tax-advantaged ways to save for retirement, consider choosing a high deductible health insurance plan and opening an HSA (Health Savings Account) if it is offered by your employer. This unique type of account is the most tax-advantaged savings vehicle available. Consider how it compares to IRAs and Roth IRAs:

Health Savings Accounts are only available to those who choose a High Deductible Health Plan. The money contributed to the HSA can be used at any time for health expenses. The account provider will send you a debit card that you can use at the pharmacy or the physician’s office. A few years ago I used HSA money to have lasik eye surgery (best decision ever). Using pre-tax money brings down the actual cost of your health care.

However, while we still fully fund our HSA, we don’t use it anymore. Instead it is one more retirement savings vehicle for us.

Unlike a Flexible Spending Account (FSA), which may also be available to you in your benefits package, any money contributed to an HSA is yours forever, and can roll over indefinitely, and you can invest the money instead of leaving it in cash. It can always be withdrawn without tax or penalty for medical expenses.

Health Savings Accounts are only available to those who choose a High Deductible Health Plan. The money contributed to the HSA can be used at any time for health expenses. The account provider will send you a debit card that you can use at the pharmacy or the physician’s office. A few years ago I used HSA money to have lasik eye surgery (best decision ever). Using pre-tax money brings down the actual cost of your health care.

However, while we still fully fund our HSA, we don’t use it anymore. Instead it is one more retirement savings vehicle for us.

Unlike a Flexible Spending Account (FSA), which may also be available to you in your benefits package, any money contributed to an HSA is yours forever, and can roll over indefinitely, and you can invest the money instead of leaving it in cash. It can always be withdrawn without tax or penalty for medical expenses.

Health Savings Accounts are only available to those who choose a High Deductible Health Plan. The money contributed to the HSA can be used at any time for health expenses. The account provider will send you a debit card that you can use at the pharmacy or the physician’s office. A few years ago I used HSA money to have lasik eye surgery (best decision ever). Using pre-tax money brings down the actual cost of your health care.

However, while we still fully fund our HSA, we don’t use it anymore. Instead it is one more retirement savings vehicle for us.

Unlike a Flexible Spending Account (FSA), which may also be available to you in your benefits package, any money contributed to an HSA is yours forever, and can roll over indefinitely, and you can invest the money instead of leaving it in cash. It can always be withdrawn without tax or penalty for medical expenses.

Four ways to check if this is a good strategy for you:

1. You and your dependents are fairly healthy and low users of healthcare beyond preventive care. 2. Your monthly cash flow is sufficient to cover medical expenses as they occur. This may mean paying out of pocket for a $125 doctor appointment if a child has an ear infection or similar costs. 3. You have an emergency fund to draw from if you encounter a larger medical issue. If someone in your family breaks a bone or needs more than preventive care, with a high deductible plan, you could owe several hundred to several thousand dollars. Any money built up in your HSA account could be used to cover it, but it is a good idea to have additional money set aside for such emergencies. 4. You are already contributing the maximum each year to your qualified retirement plan, like a 401(k), or to an IRA, and you are looking for additional ways to save with tax advantages. If the above apply to you, you might consider enrolling in a high deductible health plan, maximizing contributions to an HSA, and then NOT using the money. Pay your medical expenses out of monthly cash flow and let your HSA money grow.Consider this example of a 40-year old couple. Assume they maximize their HSA contribution ($6,900 annually, made in 12 deposits of $575), and earn an average of 6% annually on their account. At age 65 the account would be worth $398,471.52, and funds could be withdrawn without tax for health care costs.Not only that, but if you want to use the money for something other than healthcare after age 65, you just have to pay the tax. It essentially acts as an IRA at that point. Check out this article by Sarah Benner on The Slott Report’s website www.irahelp.com. Here is a key quote from that article: “Distributions that you take from your HSA after age 65 are never subject to penalty. What you use the funds for does not matter. All HSA distributions after age 65 are penalty free, even if the funds are not used for qualified health expenses. However, if you take a distribution that is not used for qualified medical expenses, it will be taxable.” Health care costs make up a significant portion of post-retirement expenses. Chances are, you will need this money for health care. This is a very tax efficient way of saving for that future need. It can be used like a 529 college savings plan is used for education expenses: money set aside in an advantaged account for a cost that you know you will one day need to cover. On the other hand, if you are lucky enough to have very low healthcare costs, you can use the money after are 65 for anything. Distributions will be treated like distributions from your IRA. Not a bad deal! Read more about HSAs in IRS Publication 969.